All Categories

Featured

Table of Contents

They typically provide an amount of insurance coverage for much less than permanent kinds of life insurance policy. Like any type of plan, term life insurance policy has benefits and downsides relying on what will work best for you. The advantages of term life include price and the capability to customize your term length and insurance coverage amount based upon your demands.

Relying on the kind of policy, term life can provide fixed premiums for the whole term or life insurance policy on level terms. The survivor benefit can be dealt with too. Due to the fact that it's a cost effective life insurance policy product and the settlements can remain the very same, term life insurance plans are popular with young individuals just starting, family members and people that desire defense for a details time period.

Decreasing Term Life Insurance Is Often Used To

You ought to consult your tax obligation consultants for your specific valid scenario. Fees show policies in the Preferred Plus Price Class problems by American General 5 Stars My agent was really experienced and handy in the procedure. No stress to get and the process was quick. July 13, 2023 5 Stars I was pleased that all my requirements were satisfied promptly and skillfully by all the representatives I talked to.

All documents was digitally completed with access to downloading and install for personal documents maintenance. June 19, 2023 The endorsements/testimonials provided must not be construed as a recommendation to buy, or an indicator of the value of any kind of item or solution. The testimonials are real Corebridge Direct customers that are not affiliated with Corebridge Direct and were not given payment.

2 Price of insurance policy rates are determined making use of approaches that vary by business. It's crucial to look at all factors when assessing the overall competition of prices and the worth of life insurance protection.

Exceptional A Whole Life Policy Option Where Extended Term Insurance Is Selected Is Called

Like the majority of team insurance policies, insurance policy plans offered by MetLife have specific exemptions, exemptions, waiting periods, reductions, restrictions and terms for keeping them in force (term life insurance for couples). Please contact your benefits administrator or MetLife for prices and complete details.

For the most part, there are two sorts of life insurance policy prepares - either term or irreversible strategies or some combination of both. Life insurers supply various forms of term plans and conventional life plans along with "passion sensitive" products which have come to be extra widespread since the 1980's.

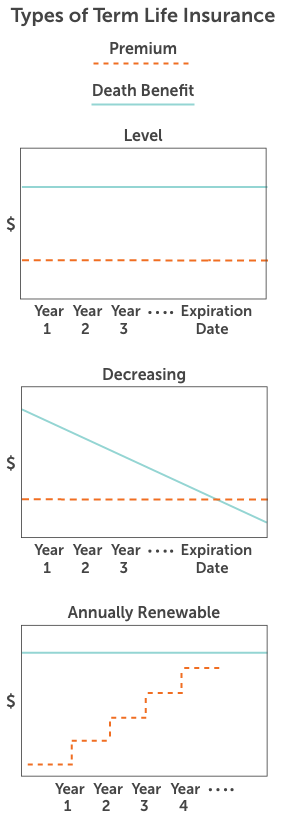

Term insurance coverage provides security for a given time period. This period can be as brief as one year or provide protection for a certain number of years such as 5, 10, twenty years or to a specified age such as 80 or sometimes approximately the oldest age in the life insurance mortality.

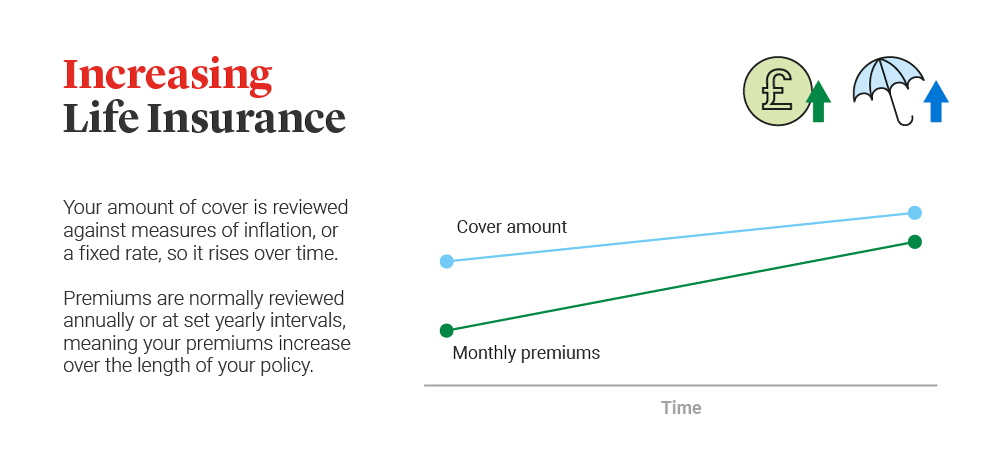

Affordable Increasing Term Life Insurance

Currently term insurance policy rates are really affordable and among the least expensive historically seasoned. It needs to be kept in mind that it is a widely held idea that term insurance policy is the least costly pure life insurance policy coverage readily available. One needs to review the plan terms carefully to determine which term life alternatives appropriate to satisfy your specific situations.

With each new term the costs is increased. The right to renew the policy without evidence of insurability is a crucial advantage to you. Or else, the risk you take is that your wellness may weaken and you may be incapable to acquire a policy at the same rates or also whatsoever, leaving you and your beneficiaries without coverage.

The length of the conversion period will vary depending on the type of term policy purchased. The costs price you pay on conversion is typically based on your "existing achieved age", which is your age on the conversion day.

Under a degree term policy the face quantity of the policy continues to be the same for the entire period. Frequently such plans are offered as mortgage protection with the amount of insurance policy decreasing as the balance of the home loan lowers.

Generally, insurers have not had the right to change costs after the plan is marketed (level term life insurance definition). Since such plans may proceed for several years, insurance companies have to make use of traditional mortality, interest and expenditure price estimates in the costs calculation. Adjustable costs insurance policy, however, enables insurers to provide insurance coverage at lower "current" premiums based upon much less conservative assumptions with the right to alter these costs in the future

Sought-After What Is Decreasing Term Life Insurance

While term insurance coverage is created to offer security for a specified period, permanent insurance is made to offer coverage for your entire life time. To keep the premium rate level, the premium at the more youthful ages surpasses the actual cost of security. This added costs constructs a get (money worth) which assists pay for the plan in later years as the expense of protection rises over the premium.

The insurance company spends the excess costs bucks This type of plan, which is often called cash worth life insurance coverage, produces a cost savings aspect. Money values are vital to an irreversible life insurance coverage policy.

Coverage-Focused A Renewable Term Life Insurance Policy Can Be Renewed

Occasionally, there is no connection between the size of the cash value and the premiums paid. It is the money value of the plan that can be accessed while the policyholder lives. The Commissioners 1980 Standard Ordinary Mortality (CSO) is the existing table used in computing minimal nonforfeiture worths and policy reserves for average life insurance policy plans.

There are 2 fundamental groups of long-term insurance policy, standard and interest-sensitive, each with a number of variants. Standard entire life policies are based upon long-lasting price quotes of expense, interest and mortality (direct term life insurance meaning).

If these quotes change in later years, the company will certainly change the costs as necessary but never over the optimum guaranteed costs specified in the plan. An economatic entire life plan offers for a standard amount of participating whole life insurance policy with an additional supplemental coverage provided with the usage of returns.

Due to the fact that the costs are paid over a much shorter span of time, the costs repayments will certainly be higher than under the whole life plan. Solitary costs whole life is limited payment life where one large superior payment is made. The plan is fully paid up and no additional costs are required.

{kind=link}

Latest Posts

Selling Final Expense Life Insurance

Omaha Funeral Insurance

Best Final Expense Companies